A Single IRS Penalty Letter Cost Me $1,400 in Unpaid Gift Tax

I opened a certified letter from the IRS last spring. The return address alone made my stomach drop. Inside was Notice CP15, a demand for $1,400 in unpaid gift tax, penalties, and interest. I had never filed a gift tax return. I didn't think I needed to. The letter explained that I had exceeded the annual gift tax exclusion in 2021 and failed to file Form 709. The penalty was $1,000; interest added another $400. I learned a hard lesson about how gift tax rules apply to everyday generosity.

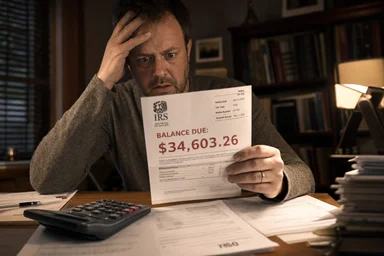

A $1,400 Surprise From the IRS

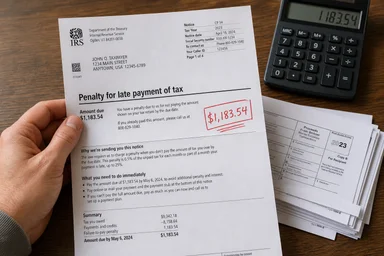

The certified letter arrived on a Tuesday. I signed for it, assuming it was something routine. Instead, the CP15 notice stated that I owed $1,400 for unpaid gift tax on transfers made in 2021. The IRS had calculated the tax based on information they already had—likely from bank records and other filings. I had never received a notice like this before. My first thought was that someone had stolen my identity. But the letter referenced my specific Social Security number and the exact amounts I had transferred.

The breakdown was simple: a failure-to-file penalty of $1,000, plus interest of $400. The underlying tax itself was small—$0 in this case because my gifts fell below the lifetime exemption—but the penalty for not filing Form 709 was substantial. I had given $10,000 to a friend for a down payment on a house and paid $5,000 directly to a hospital for a relative's medical bill. I thought both were exempt or below the threshold. I was wrong.

The IRS had matched my bank records against their database and flagged the $10,000 transfer as a gift. They assumed the medical payment was also a gift, even though medical payments made directly to a provider are exempt. I had missed the exemption because I didn't file the proper forms. The penalty snowballed quickly.

How Gift Tax Works for Ordinary People

Gift tax is a federal tax on transfers of money or property where you don't receive full value in return. Most people assume it only affects the wealthy. In 2021, the annual exclusion was $15,000 per recipient. That means you could give up to $15,000 to any number of people without filing a gift tax return. Gifts above that amount require filing Form 709, even if no tax is due.

The lifetime exemption in 2021 was $11.7 million per person. That means you could give away up to that amount over your lifetime without paying gift tax, but you still have to report gifts exceeding the annual exclusion. The filing requirement is separate from the tax liability. Many people, including me, assume they will never trigger it because their total gifts are small. But the IRS doesn't care about your total; it cares about each recipient.

The annual exclusion applies per recipient per year. If you give $16,000 to one person, you must file Form 709 for the $1,000 excess. The excess reduces your lifetime exemption. If you've never given large gifts, your exemption remains intact. But the filing requirement is mandatory. Ignoring it triggers penalties.

Some financial advisors argue that the gift tax system is designed to catch only the wealthy, but the IRS uses automated matching to flag unreported gifts. As of late 2024, the annual exclusion has risen to $18,000, but the rules remain the same. The threshold is higher, but the filing requirement still applies to any gift above that amount.

The Mistake: Overlooking Small Gifts

In 2021, I gave $10,000 to a friend to help with a down payment. I considered it a loan, but we had no written agreement and no interest. The IRS views such transfers as gifts unless you have a formal loan with a market-rate interest and a repayment schedule. I didn't. That $10,000 was a gift.

I also paid $5,000 directly to a hospital for a relative's medical bill. Medical payments made directly to a provider are exempt from gift tax, regardless of amount. I knew that, but I didn't file Form 709 to report the exemption. The IRS doesn't automatically know the purpose of a payment. When they saw a $5,000 transfer to a hospital, they flagged it as a gift. I had to prove it was a medical payment, which required filing an amended return.

The Vanguard mutual fund fee taught me that small percentages can cost thousands over time. Similarly, small gifts can trigger penalties that dwarf the original amount. The $15,000 annual exclusion is per recipient, not per gift. If you give $10,000 to one person and $6,000 to another, you're below the threshold for each. But if you give $16,000 to one person, you exceed it.

I had given $10,000 to my friend and $5,000 for the medical bill—total $15,000. But the medical payment was exempt, so my reportable gift was $10,000, which is below $15,000. I didn't need to file Form 709 for the gift to my friend. However, the IRS didn't know about the medical exemption because I hadn't filed anything. They assumed both were gifts and that I had exceeded the annual exclusion for two separate recipients.

IRS Notice CP15: What It Actually Says

Notice CP15 is a demand for payment of a failure-to-file penalty for gift tax returns. The penalty is 5% of the tax due per month, up to 25%. In my case, the tax due was $0 because my gifts were under the lifetime exemption, but the IRS calculated a penalty based on the assumption that I owed tax. The math was confusing: a penalty on zero tax? The IRS explained that the penalty is based on the "net tax due" as if you had filed, but since the tax was zero, the penalty was a flat $1,000 for late filing.

Interest accrues on the unpaid tax from the original due date. The tax due was $0, but the penalty itself accrues interest. The IRS charged $400 in interest on the $1,000 penalty, bringing the total to $1,400. The notice gave me 21 days to pay or dispute. I called the IRS and spent two hours on hold. The representative confirmed that if I filed Form 709 showing the medical exemption, the penalty might be abated.

The CP15 notice is automated. It's triggered when the IRS's computer system detects a mismatch between reported gifts and bank records. The system doesn't consider exemptions or exclusions. It simply flags any transfer over $15,000 to a single recipient. The burden is on you to prove the exemption. The notice is not an audit; it's a computer-generated demand.

Some tax professionals criticize the CP15 process for being too aggressive. The IRS sends these notices without any human review. If you ignore them, they escalate to liens and levies. But if you respond promptly, you can often get the penalty waived, especially if you have a reasonable cause, such as misunderstanding the rules.

Why the System Catches Small Filers

The IRS uses the Document Matching Program to compare information returns—like bank reports of large transfers—with tax returns. If you transfer more than $15,000 to someone in a single transaction, the bank may report it. The IRS then checks whether you filed a gift tax return. If not, you get a CP15. The system is designed to catch unreported income, but it also catches unreported gifts.

Small filers are more likely to be caught because they are less likely to have professional preparers. A CPA would have noticed the gift and filed Form 709 proactively. I prepared my own taxes and missed the requirement entirely. The automated notice arrived within 18 months of the gift, which is typical. The IRS's computer doesn't distinguish between a gift and a loan or between a medical payment and a cash transfer.

The T-Mobile phone insurance story showed how fine print can nullify a claim. Similarly, the fine print of gift tax rules can nullify your assumption that small gifts are safe. The annual exclusion is generous, but the filing requirement is strict. The IRS's automated system ensures that even small oversights are penalized.

Some critics argue that the system is unfair to ordinary people who make one-time gifts. The annual exclusion hasn't kept pace with inflation in some years, and the $15,000 limit in 2021 was only slightly above the average down payment assistance. But the rules are the rules. The IRS expects compliance, and ignorance is not a defense.

How to Avoid This Trap

Track all gifts over $10,000 per person. Even if you're below the annual exclusion, keeping a record helps. If you make a gift over $15,000 to one person, file Form 709 by April 15 of the following year. The form is straightforward: you list the recipient, the amount, and any exemptions. You don't need to pay tax unless you've exhausted your lifetime exemption.

Use direct payments for tuition or medical bills. Payments made directly to an educational institution or medical provider are exempt from gift tax, regardless of amount. But you must document them. If the IRS asks, you need proof that the payment went directly to the provider, not to the individual.

Set a calendar reminder before April 15. Gift tax returns are due on the same date as income tax returns. If you file an extension for your income tax, it also extends the gift tax return deadline. But if you miss the deadline, the penalty clock starts. The penalty for late filing is 5% per month on the tax due, capped at 25%. Even if no tax is due, the penalty can be $1,000 or more.

Consult a CPA if you give more than $15,000 to any person in a year. The cost of a professional review is far less than the penalty. Many CPAs will file Form 709 for a few hundred dollars. The life insurance cash value article showed how hidden fees can erode value. Similarly, ignoring gift tax rules can erode your savings through penalties.

Lessons From a Costly Oversight

Gift tax rules apply to everyday generosity. A gift to a friend for a down payment, a payment for a relative's medical bill, or even a large holiday check can trigger the filing requirement. The annual exclusion is generous, but the filing requirement is not optional.

One missed form can snowball into thousands of dollars in penalties and interest. In my case, the underlying tax was $0, but the penalty was $1,000 and interest was $400. The total cost of my oversight was more than the original gift. The IRS waived the penalty after I filed Form 709 and proved the medical exemption, but I still paid $400 in interest.

The penalty letter taught me to stay vigilant. I now track all gifts over $10,000 and set a reminder to file Form 709 if needed. I also keep records of direct payments for medical and tuition expenses. The system is automated and unforgiving, but with a little planning, you can avoid the trap.

Some people argue that the gift tax should be simplified or abolished, but until that happens, compliance is the only safe path. The IRS's computer doesn't care about your intentions. It only cares about the numbers. A single oversight can cost you thousands.

Real-World Scenarios and Trade-Offs

Consider a parent who gives $20,000 to their adult child for a wedding. In 2021, that exceeds the annual exclusion by $5,000. The parent must file Form 709 for that $5,000 excess. If they fail to file, they could face a penalty similar to mine. However, if the parent pays the wedding venue directly, that payment is exempt as a gift for tuition? No, wedding expenses are not exempt like medical or tuition payments. This distinction is crucial. Many people assume all gifts to family are exempt, but only specific categories qualify.

Another example: a grandparent pays $30,000 directly to a university for a grandchild's tuition. That is exempt regardless of amount. But if the grandparent gives the money to the grandchild to pay tuition, it's a gift subject to the annual exclusion. The trade-off is control versus tax compliance. Direct payment to the provider avoids filing, but it also means you lose the ability to change your mind or use the funds for other purposes.

Some people might argue that the annual exclusion should be per donor per couple, not per recipient. Married couples can split gifts, effectively doubling the exclusion to $30,000 per recipient in 2021. This is a powerful strategy for those who plan to make large gifts. But it requires filing Form 709 even if the gift is under the doubled limit, because gift splitting must be reported. The trade-off is more paperwork for a higher threshold.

There's also a counter-argument that the IRS's automated system creates a burden on honest taxpayers. The system is designed to catch tax evasion, but it catches innocent mistakes too. Some tax experts recommend that the IRS increase the threshold for automated CP15 notices to $20,000 or more, reducing false positives. However, as of now, the threshold remains at $15,000. Taxpayers must be proactive.

Another scenario: a person lends $20,000 to a friend with a written agreement and charges 2% interest, which is below the applicable federal rate (AFR). The IRS may treat the forgone interest as a gift. This is a common trap for informal loans. The trade-off is that you can structure a loan with proper interest to avoid gift tax, but you must document it and report the interest income. It's more complex but avoids penalties.

Finally, consider the impact of state gift taxes. Some states have their own gift tax with lower exemptions. For example, Connecticut has a gift tax exemption of $9.1 million in 2024, but other states like New York do not have a gift tax. Taxpayers in states with a gift tax must file both federal and state returns, doubling the compliance burden. This adds another layer of complexity for those living in or gifting to residents of such states.

Disclaimer: This article is for informational purposes only and does not constitute professional tax advice. Consult a qualified tax professional for your specific situation.