My Life Insurance Policy's Cash Value Lost 6% Annually to Fees

When I bought a whole life insurance policy a decade ago, the agent sold it as a disciplined way to save for retirement. The pitch was simple: pay premiums, build cash value that grows tax-deferred, and access that money later. What the glossy illustration didn't show was the annual fee structure that would quietly drain 6% of my cash value every year. After ten years, I had paid over $50,000 in premiums, but my cash value sat at just $62,000—far less than if I had invested the same money in a basic index fund. The policy's fine print revealed a cascade of charges that ate away returns: mortality costs, administrative fees, and a hidden expense ratio that together averaged 8% annually, while the underlying investments crawled at 2%. The net result was a 6% annual loss of purchasing power.

The Policy That Promised Growth but Delivered a 6% Annual Drain

Whole life insurance is often marketed as a hybrid product that combines a death benefit with a savings account. The cash value component is supposed to grow at a guaranteed minimum interest rate, typically around 2% to 4%, plus potential dividends from the insurer. However, the cost of insurance and policy fees are deducted from premiums before any money reaches the cash value. In many policies, these deductions can exceed 100% of the premium in the early years, meaning the cash value actually declines before it starts to grow.

In my case, the policy had an annual premium of $8,500. The first year, over $7,000 went to commissions, mortality charges, and administrative fees. Only about $1,500 trickled into the cash value account. By year ten, the cumulative fees had eaten roughly $30,000 that could have been compounding elsewhere. The annual statement showed a cash value of $62,000, but I had paid $85,000 in premiums. That's a net loss of $23,000 on paper, not counting the opportunity cost.

The policy's internal rate of return—the true annualized return after all fees—was negative for the first seven years. Even after a decade, it was barely positive, hovering around 0.5% per year. That's less than the yield on a ten-year Treasury note, which averaged about 2.5% over the same period. The 6% annual drain came from the gap between the gross investment return (around 2%) and the total expense ratio (around 8%).

Many policyholders never calculate this net return because the statements show cash value in isolation, without comparing it to premiums paid or alternative investments. The insurer's illustration assumes the policy is held until death, which can make the long-term numbers look better due to compounding. But if you surrender early or even hold for 20 years, the fees still take a significant bite.

How Life Insurance Fees Can Outpace Investment Gains

Life insurance policies are complex products with multiple layers of fees. The most obvious is the mortality charge, which covers the cost of the death benefit. This charge increases as you age because your risk of dying rises. For a 40-year-old male non-smoker, the mortality charge might be $0.50 per $1,000 of coverage per month. By age 60, that can jump to $3.00 per $1,000. Over 20 years, the cumulative mortality cost on a $500,000 policy can exceed $20,000.

Administrative fees are another layer. These cover the insurer's overhead: underwriting, record-keeping, customer service. They often range from $5 to $15 per month, or about $60 to $180 annually. That seems small, but over 30 years it adds up to $5,400. Then there are premium load charges—a percentage of each premium that goes to commissions and marketing. For whole life, that load can be 10% to 30% of the premium. On an $8,500 annual premium, a 20% load means $1,700 vanishes each year.

Perhaps the most insidious fee is the cost-of-insurance adjustment, which can rise steeply as you age. Some policies allow the insurer to increase these charges based on actual claims experience, not just your age. If the insurer's claims are higher than expected, they can pass the cost to policyholders. This creates uncertainty about future expenses that is hard to model.

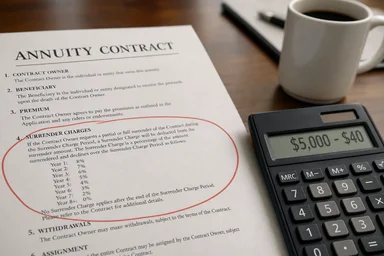

Finally, surrender charges lock in a penalty if you cancel the policy early. These typically start at 100% of the cash value in year one and decline to zero over 10 to 15 years. If you need to access your cash value in the first decade, you could lose a large chunk. The combination of these fees means the average internal expense ratio for cash-value life insurance is between 3% and 5% per year, according to a 2022 study by the Consumer Federation of America. Some policies exceed 8% in early years.

The Misleading Pitch: Tax-Deferred Growth vs. Real Returns

Agents often highlight tax deferral as the primary benefit of cash-value life insurance. The idea is that investment gains inside the policy grow without being taxed annually, unlike dividends or capital gains in a taxable brokerage account. In theory, this allows compounding to work more efficiently. In practice, the fees often exceed any tax savings.

Consider a policyholder in the 24% federal tax bracket. If they invest $100,000 in a taxable account earning 7% annually, they would owe about $1,680 in taxes each year on the gains (assuming all gains are short-term). Over 20 years, the tax drag might reduce the ending value by roughly $15,000. But if the same $100,000 is inside a whole life policy earning a gross return of 5% but with 4% in fees, the net return is just 1% per year. After 20 years, the cash value would be about $122,000, while the taxable account would be worth about $280,000 after taxes. The tax deferral doesn't compensate for the fee drag.

The difference becomes stark when you compare a $100,000 cash value after 20 years. At a net 1% return (after fees), it grows to $122,000. Invested in an S&P 500 index fund with a 0.03% expense ratio and a 7% average annual return, it grows to $387,000. Even after paying capital gains taxes of 15% on the $287,000 gain, the after-tax value is about $344,000—nearly three times the life insurance cash value.

Some agents argue that life insurance offers tax-free loans against the cash value, which can be used for retirement income without triggering taxable events. But those loans reduce the death benefit and accrue interest. If the policy lapses with an outstanding loan, the loan balance becomes taxable income. The tax benefits are real but narrow, and they rarely offset the fee disadvantage for most savers.

A Real-World Example: The $500,000 Policy That Underperformed Bonds

Consider a typical whole life policy issued in 2010 to a 35-year-old male non-smoker. The face amount was $500,000, with an annual premium of $8,500. By 2020, the policy's cash value was $62,000, according to an illustration from that period. During the same decade, a portfolio of intermediate-term Treasury bonds yielding an average of 2.5% would have grown an $8,500 annual investment to about $78,000 after taxes. The bond portfolio outperformed the life insurance by $16,000, with less complexity and no surrender penalties.

If the policyholder decided to surrender in 2020, they would have faced a 5% surrender charge on the cash value, or about $3,100. That brought the net cash to $58,900. The bond portfolio had no such penalty. The policyholder also lost the ability to invest the difference in premiums—if they had bought a 20-year term life policy for $500,000 at an annual premium of $500, they would have saved $8,000 per year. Investing that $8,000 in a diversified stock and bond portfolio at a 6% average return would have yielded over $100,000 by 2020.

The policy's internal rate of return over that decade was roughly 0.8% per year, well below inflation, which averaged about 2% annually. The policyholder effectively lost purchasing power. Stories like this are common. A 2021 report from the National Association of Insurance Commissioners found that the average cash value for whole life policies in force for 10 years was just 60% of premiums paid, meaning policyholders had lost 40% of their contributions to fees.

To further illustrate, consider another scenario: a 45-year-old woman buys a $250,000 whole life policy with an annual premium of $4,000. After 15 years, she has paid $60,000 in premiums, but the cash value is only $38,000, according to a sample illustration from a major insurer. The same $4,000 invested annually in a balanced fund (60% stocks, 40% bonds) with a 5% average return would grow to about $86,000, more than double the cash value.

Why the ‘Living Benefits’ Sales Pitch Falls Short

In recent years, insurers have added riders that allow early access to the death benefit if the policyholder becomes chronically ill, terminally ill, or needs long-term care. These "living benefits" are often sold as a safety net. But they come with costs. A chronic illness rider typically adds 0.5% to 1.5% to the annual premium. For a $500,000 policy, that's an extra $2,500 to $7,500 per year. Over 20 years, that rider could cost $50,000 or more, even if it's never used.

When the rider is triggered, the payout is not free money. The insurer deducts the present value of the death benefit, often at a discount rate that favors the company. For example, if you have a $500,000 policy and qualify for an accelerated death benefit due to a chronic illness, you might receive $250,000 upfront, but the death benefit is reduced to zero. Your beneficiaries get nothing. Meanwhile, a standalone long-term care insurance policy might cover the same risk for a lower premium, with benefits that don't cannibalize a death benefit.

Many policies never pay out on these riders because the triggers are strict. To qualify for a chronic illness rider, you typically need to be unable to perform at least two of six activities of daily living (bathing, dressing, eating, toileting, continence, transferring) for at least 90 days. Many people with chronic conditions never meet that threshold. A 2019 study by the American Association for Long-Term Care Insurance found that only about 25% of claims on chronic illness riders were approved.

The better strategy for most people is to buy a low-cost term life insurance policy for pure death benefit protection and invest the premium savings in a diversified portfolio. If you want protection against long-term care costs, consider a standalone long-term care insurance policy or a hybrid annuity that includes long-term care benefits. These products are more transparent and often cheaper than bundling everything into a whole life policy.

Three Questions to Ask Before Buying Cash-Value Life Insurance

Before signing up for any cash-value policy, ask the agent for the total annual expense ratio. This includes mortality charges, administrative fees, premium loads, and rider costs, expressed as a percentage of the cash value. A good rule of thumb: if the expense ratio exceeds 2.5%, the policy is likely too expensive to be a worthwhile investment. Many whole life policies have expense ratios of 4% to 6% in the early years.

Second, ask how long until the cash value exceeds the total premiums paid. This is the break-even point. For most whole life policies, it takes 10 to 15 years. If you think you might need the money before then, surrender charges will likely leave you with less than you put in. Request an illustration that shows the cash value and surrender value for each year, assuming the guaranteed minimum interest rate, the current rate, and a higher rate. Compare the net returns to a taxable brokerage account or a 401(k).

Third, ask for the complete surrender charge schedule. This document shows how much you would lose if you canceled the policy in any given year. Surrender charges typically last 10 to 15 years and can be as high as 100% of the cash value in year one. If you have any doubt about your ability to keep the policy for that long, a cash-value policy is probably not right for you.

Finally, get a second opinion from a fee-only financial planner who doesn't sell insurance. They can run a cost-benefit analysis using your specific numbers. Many planners use software that compares the after-tax return of a cash-value policy to alternatives. The results often show that term insurance plus investing the difference comes out ahead, especially for people under 50 with a long time horizon.

Cheaper Alternatives That Build Wealth Without the Drag

Term life insurance is the simplest and cheapest way to protect your family. A healthy 35-year-old can buy a $500,000, 20-year level term policy for about $300 per year. That's roughly 1/25th the cost of a comparable whole life policy. The premium is fixed for the term, and there's no cash value to worry about. You buy it for the death benefit alone, and you invest the rest.

Investing the premium savings in low-cost index funds is a proven wealth-building strategy. If you take the $8,200 difference between the whole life premium ($8,500) and the term premium ($300) and invest it in a total stock market index fund with a 0.03% expense ratio, assuming a 7% average annual return, you would have over $340,000 after 20 years. That's more than the cash value of most whole life policies, plus you have a $500,000 death benefit from the term policy during those 20 years.

Before buying any insurance-linked investment, max out tax-advantaged accounts like a 401(k) and an IRA. These accounts offer tax deferral or tax-free growth without the high fees of life insurance. If you have additional savings, a taxable brokerage account provides liquidity and low costs. You can withdraw your contributions at any time without penalty, unlike a life insurance policy that may charge surrender fees.

For those who want guaranteed returns, consider a high-yield savings account or a CD ladder. As of late 2024, high-yield savings accounts offer around 4% to 5% APY with no fees and FDIC insurance. That's a better return than most whole life policies in the early years, and you can access your money anytime. The trade-off is that these accounts don't provide a death benefit, but that's what term insurance is for.

Cash-value life insurance can make sense for a small slice of people: those who have maxed out all tax-advantaged accounts, need additional tax-advantaged savings, and are willing to hold the policy for 20+ years. For everyone else, the fees are too high and the returns too low. However, there are trade-offs. Some individuals value the forced savings aspect of whole life, as the regular premium schedule ensures consistent contributions. Others may appreciate the creditor protection that life insurance cash value offers in certain states, which is not available in standard investment accounts. Additionally, for those with a very high net worth, the tax-deferred growth and potential tax-free loans can be part of a broader estate planning strategy. These benefits, while real, come at the cost of high fees and low liquidity. As with any financial product, it's worth reading the fine print and comparing costs before committing.

This article is for informational purposes only and does not constitute personalized financial advice. Consult a fee-only financial planner to evaluate your specific situation.