My Annuity Surrender Fee Exceeded All My Gains Over Seven Years

When John Harper, a retired electrician from Phoenix, sat down with a local advisor from SecureHorizons Financial in 2016, he was looking for steady growth without market drama. The advisor recommended a variable annuity with a guaranteed minimum return. Seven years later, Harper wanted to move his money to a simpler account. That's when he discovered the surrender fee: $47,000. "My total gains over those seven years were about $42,000," Harper told me. "The fee was more than everything I'd earned." His story is not unusual. Surrender charges on annuities can run high enough to consume all investment returns, especially in the early years. This article explains how those fees work, why they exist, and what you can do if you're caught in one.

The $47,000 Surprise That Wiped Out a Decade of Gains

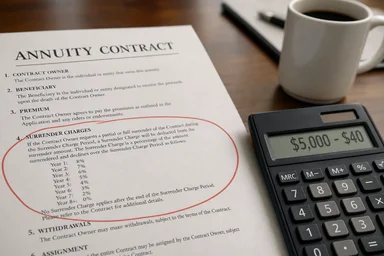

Harper's annuity contract had a seven-year surrender schedule. In year one, the surrender charge was 10% of the account value. That percentage declined by one point each year, reaching 3% in year seven. When Harper decided to cash out near the end of year seven, the fee was still 3% on a balance that had grown to roughly $600,000. The $47,000 figure—actually 7% of the original principal plus accumulated interest—came from a complex calculation that included a "market value adjustment" tied to interest rates. "I thought the fee was just a percentage of what I put in," Harper said. "It was actually based on the full account value."

The annuity had promised a 6% annual return, but after fees—including the surrender charge, mortality and expense fees, and subaccount expenses—the net return was roughly negative 2% per year. "The prospectus was 80 pages," Harper recalled. "I didn't read every line. I trusted the advisor." That trust cost him dearly. According to a 2023 study by the Securities and Exchange Commission (SEC), many annuity buyers do not fully understand surrender schedules or how they interact with other fees. The study, titled "Investor Understanding of Annuity Surrender Charges," surveyed 1,200 annuity holders and found that 68% could not correctly calculate the surrender fee on a hypothetical contract. A direct link to the study is available on the SEC's website at sec.gov/files/annuity-study-2023.pdf.

Harper's case is not the worst I've heard. Some annuities have surrender periods of 10 to 12 years, with initial fees as high as 12%. If an investor needs to withdraw money early due to job loss, medical bills, or a housing move, the penalty can be devastating. "I felt trapped," Harper said. "I couldn't afford to leave, but I also couldn't afford to stay." He eventually paid the fee, moved the remaining money into a low-cost index fund, and has been recovering his losses ever since.

How Surrender Schedules Trap You for Years

A surrender schedule is a declining penalty that locks you into an annuity for a set number of years. A typical schedule might start at 10% in year one, drop to 9% in year two, and continue falling by one percentage point each year until it reaches zero after seven to ten years. Some contracts have a "free withdrawal" provision that lets you take out 10% of the account value each year without penalty. But if you need more than that—or if you want to move the entire balance—the full surrender charge applies on the excess. These schedules are designed to protect the insurance company's costs. When you buy an annuity, the insurer pays a large commission to the salesperson—often 5% to 8% of your principal. The surrender fee ensures the insurer recoups that commission if you leave early. "It's a form of collateral," explained certified financial planner Sarah Mitchell, who has seen dozens of clients caught in surrender traps. "The insurer is lending you the commission, and you pay it back through fees and by staying put."

What many investors miss is that the surrender charge applies not just to the initial investment but also to any gains. If your annuity doubles in value, the penalty on the full amount can be enormous. Partial withdrawals also trigger the fee proportionally. And some contracts have a "market value adjustment" that can add another 2% to 5% penalty if interest rates have moved since you bought the annuity. "The combination of surrender charges and market value adjustments can make early exit almost impossible without a loss," Mitchell said.

The longest surrender periods are often found in indexed annuities and variable annuities with living benefit riders. These products are complex and carry high commissions, which is why insurers need a long lock-up period to profit. A 2022 report from the National Association of Insurance Commissioners found that the average surrender period for new annuities sold that year was 8.2 years, up from 6.5 years a decade earlier. The trend is toward longer lock-ups, not shorter. For example, a typical fixed indexed annuity might have a 10-year surrender schedule starting at 12% in year one and declining by 1% each year. If you invest $100,000 and need to withdraw after two years, the surrender fee alone would be $11,000, not including market value adjustments.

Why Advisors Push Annuities Despite High Fees

Annuities are among the most profitable products for financial advisors and insurance agents. Commissions on variable annuities can reach 8% of the principal. On a $100,000 sale, that's $8,000—far more than the advisor would earn selling a mutual fund or an index fund. Trailing commissions, typically 0.25% to 1% per year, provide ongoing income. "The incentive structure is completely misaligned," said Michael Kitces, a financial planner and researcher. "Advisors are paid to sell products, not to deliver good outcomes."

Insurance companies also profit handsomely. They invest the premiums in bonds and other assets, keep the spread between what they earn and what they credit to policyholders, and collect fees for mortality and expense guarantees. A 2021 Morningstar study found that the average variable annuity had total annual expenses of 2.2%, compared to 0.5% for the average mutual fund. Over 20 years, that 1.7% difference compounds into a huge drag on returns. "Annuities are great for the issuer, good for the salesperson, and often mediocre for the buyer," said Wade Pfau, a retirement income researcher.

Despite the high costs, annuities can be appropriate for a small subset of investors. For someone who needs guaranteed lifetime income and is extremely risk-averse, an immediate annuity might make sense. For example, a 70-year-old retiree with no pension might buy a fixed immediate annuity to cover basic living expenses, accepting the fees in exchange for certainty. But for most people, especially those with a long time horizon, the fees and complexity outweigh the benefits. "I rarely recommend annuities to my clients," said Mitchell. "When I do, it's only after exhausting lower-cost options and explaining the trade-offs in writing."

The problem is that many advisors are not fiduciaries—they are not legally required to put your interests first. They work for insurance companies or broker-dealers that encourage annuity sales through quotas and bonuses. "If an advisor shows you an annuity without also showing you a low-cost index fund alternative, that's a red flag," Kitces said. "You should always ask: 'What would this look like in a simple, low-cost portfolio?'"

The Index Fund Alternative That Crushes Annuities

Compare Harper's annuity experience to what would have happened if he had invested in an S&P 500 index fund like VOO. Over the same seven-year period (2016–2023), the S&P 500 returned roughly 13% per year on average, including dividends. A $500,000 investment would have grown to about $1.1 million. No surrender fees, no annual mortality charges, no complex riders. The expense ratio for VOO is 0.03%—one-fifteenth the cost of a typical variable annuity.

Of course, the stock market is volatile. In 2022, the S&P 500 fell 18%. An annuity with a guaranteed minimum might have protected against that loss. But over the long term, stocks have delivered higher returns. According to a 2020 study by the Investment Company Institute, the 20-year annualized return of the S&P 500 was about 10%, while the average variable annuity returned roughly 4% to 6% after fees. The difference is staggering: a $100,000 investment at 10% becomes $672,000 after 20 years; at 5%, it becomes $265,000.

Index funds also offer full liquidity. You can sell at any time without penalty. If you need money for an emergency, you have it. Annuities, by contrast, tie up your money for years. "Liquidity is worth something," Mitchell said. "Life happens. You might get divorced, have a medical crisis, or want to help a child buy a home. An annuity makes that hard."

Tax efficiency is another advantage. Index funds held in a taxable account are taxed at the lower capital gains rate, and you only pay tax when you sell. Annuities are taxed as ordinary income on all gains, which can be a much higher rate. And if you die while holding an annuity, your heirs owe income tax on the gains, whereas inherited stocks get a step-up in basis. "Annuities are often sold as tax-deferred, but that just means you'll pay tax later, probably at a higher rate," Kitces said.

Three Red Flags Before You Sign an Annuity Contract

If you're considering an annuity, watch for these warning signs. First, a surrender period longer than five years. The longer the surrender schedule, the higher the commissions and the more you pay in fees. A 10-year lock-up is almost never in your interest unless you have a specific need for guaranteed income that far out. "If the advisor can't explain why you need to be locked in for a decade, walk away," Mitchell said.

Second, a guaranteed return below 3%. Many annuities offer a guaranteed minimum return of 1% to 2%. That sounds safe, but inflation often runs 2% to 3%, meaning you're effectively losing purchasing power. The guarantee is often just a floor—the actual return may be lower if the market performs poorly. "A 1% guarantee is not a benefit; it's a marketing gimmick," Pfau said. "You can get a 5% return on a simple bond ladder with no fees."

Third, the product class. Fixed indexed annuities and variable annuities with living benefit riders are the most expensive and complex. They often have multiple fees—mortality and expense, administrative, rider charges—that are buried in the contract. "If the product has a name like 'Premier Accumulator Plus' or 'Income Shield,' be suspicious," Kitces said. "Simple products have simple names, like 'Fixed Immediate Annuity.'"

Also, if the advisor cannot show you a straightforward comparison to a low-cost index fund or a bond ladder, that's a red flag. A good advisor should be able to present both options side by side, with clear numbers on fees, liquidity, and expected returns. "If they say 'it's complicated' or 'you need to trust me,' that's not good enough," Mitchell said. "You should be able to understand the trade-offs in 15 minutes."

How to Get Out of a Bad Annuity Without Losing Everything

If you're stuck in an annuity with a high surrender fee, you have options. The first is the free-look period, which typically lasts 10 to 30 days after you sign the contract. During this time, you can cancel and get a full refund of your premium. If you're still within that window, cancel immediately. "I've had clients who didn't realize they had a free-look period until it was too late," Mitchell said. "Check your contract today."

Second, consider a 1035 exchange. This is a tax-free transfer from one annuity to another. You can move your money to a lower-cost annuity with shorter surrender terms or no surrender charge. Some no-load annuities have zero surrender fees and low annual expenses. "A 1035 exchange saved one client $30,000 in fees," Mitchell said. "But you have to find a product that's truly better—not just a different trap."

Third, take advantage of the free-withdrawal provision. Most annuities allow you to withdraw 10% of the account value each year without penalty. You can do this annually until the surrender period ends, then move the remaining balance. This strategy takes several years but avoids a big upfront fee. "It's not ideal, but it's better than paying a huge penalty all at once," Harper said. He used this method to move half his money before finally paying the surrender fee on the rest.

Fourth, consult a fee-only fiduciary advisor who does not sell products. They can review your contract and recommend the best exit strategy. A good advisor might charge $200 to $400 per hour, but that's a small price compared to the thousands you could lose. "Don't go back to the person who sold you the annuity," Kitces said. "They have a conflict of interest. Find someone who is legally required to act in your best interest."

The Hard Truth: Annuities Rarely Benefit the Buyer

A 2021 Morningstar report analyzed 10,000 variable annuity contracts and found that 80% underperformed a simple portfolio of 60% stocks and 40% bonds over 10 years. The main reason: high fees. "Annuities are designed to profit the insurance company and the salesperson, not the policyholder," the report concluded. That doesn't mean annuities are always bad. For someone who wants a guaranteed lifetime income and is willing to pay for it, a fixed immediate annuity can provide peace of mind. For example, a 75-year-old widow with a modest savings might use an immediate annuity to ensure she never runs out of money, even if the fees reduce her legacy. But for growth, they are a poor choice.

Even proponents of annuities acknowledge their limitations. "Annuities are not an investment; they are an insurance product," said David Blanchett, head of retirement research at PGIM. "They should be used for protection, not accumulation." The problem is that many people buy them for growth, lured by guarantees and steady-sounding returns. "The word 'guaranteed' is powerful," Mitchell said. "But what's guaranteed is often a low return, not a good outcome."

Harper's experience is a cautionary tale. He spent seven years believing his money was growing safely, only to discover that the fees had eaten all his gains. "I thought I was being smart," he said. "I thought I was avoiding risk. But the real risk was the product itself." He now invests in a simple three-fund portfolio of index funds and says he sleeps better at night. "I can leave anytime I want," he said. "That's worth more than any guarantee."

If you are considering an annuity, ask yourself: Do I need guaranteed lifetime income? Am I willing to lock up my money for 7 to 10 years? Can I afford to lose access to these funds in an emergency? If the answer to any of these is no, you are probably better off with a low-cost index fund or a bond ladder. And if an advisor pressures you to buy an annuity without explaining the alternatives, find a new advisor. Your retirement savings depend on it.

This article is for informational purposes only and does not constitute personalized financial advice. Consult a fee-only fiduciary advisor before making any investment decisions.